Quarterly Economic Update

Second Quarter 2026

The second quarter of 2026 demonstrated an important lesson for investors: markets can continue to advance even when uncertainty dominates the headlines. Persistent inflation concerns, heightened geopolitical tensions, high energy prices, and evolving expectations for Federal Reserve policy all contributed to periods of market volatility. Despite these headwinds, U.S. equities recovered from a difficult first quarter and continued their longer-term upward trend, leaving the major market indices higher after the first half of the year.

Led by strong corporate earnings, a resilient U.S. economy, and continued enthusiasm for artificial intelligence (AI) and technological innovation equity markets made new highs during the quarter. Both the S&P 500 and Dow Jones Industrial Average (DJIA) indexes experienced healthy gains as the S&P 500 closed the quarter up 14.4% and the DJIA gained approximately 12.8%. Through the first six months of 2026, the S&P 500 has gained 9.6%, and the Dow has advanced 8.9%. (Source: apnews.com; statmuse.com 6/30/26)

One of the most important drivers of equity markets is the direction of corporate America – and it continued to deliver solid results. According to FactSet, on June 26, the estimated year-over-year growth for S&P 500 companies is 23.1%, which would mark the seventh consecutive quarter of double-digit earnings increases and the second-straight quarter of earnings growth over 20%.

The energy sector was among the largest contributors to market volatility. West Texas Intermediate (WTI) crude oil experienced a 74% volatility rate as it swung between the high $60s and the low $120s per barrel during the quarter. Meanwhile, the U.S. labor market continued to demonstrate resilience as the U.S. Bureau of Labor Statistics stated the unemployment rate remained steady at 4.3% in May.

Overall, the second quarter reinforced an important investment principle: while headlines often create short-term market volatility, long-term market performance is ultimately driven by healthy, long-term focused fundamentals. While volatility remains a normal part of investing, the quarter reinforced the importance of focusing on long-term fundamentals rather than reacting to short-term market noise. As financial professionals, our role is to closely monitor market developments and help ensure your portfolio remains aligned with your broader financial goals.

Inflation & Interest Rates

Key Points:

- The Federal Reserve left the federal funds rate unchanged during the second quarter of 2026, maintaining the target range at 3.50%–3.75% but they reduced expectations for rate cuts and discussed the possibility of future rate increases.

- Inflation remains above the Fed's long-term target and continues to be a concern.

At the April FOMC meeting, the final meeting chaired by Jerome Powell, the Federal Reserve held interest rates steady. At the June meeting, the first under newly appointed Federal Reserve Chair Kevin Warsh, policymakers again voted to maintain the target rate range of 3.50%–3.75%, while signaling a more hawkish outlook for the remainder of the year. (Source: CNBC, June 17, 2026)

Consumer spending also remains healthy. According to May data from the Bureau of Labor Statistics, the core Consumer Price Index (CPI), which excludes food and energy, increased 2.9% year-over-year. Geopolitical developments should continue to affect energy prices and therefore they will also influence inflation trends. (Source: Bureau of Labor Statistics)

Looking ahead, currently the prospect of a rate cut in 2026 appears increasingly unlikely. In fact, the possibility of a rate increase later this year has gained momentum. The path forward will largely depend on the trajectory of inflation, labor market conditions, and overall economic growth. Interest rates and inflation remain critical factors in financial planning and investment decision-making so we will continue to monitor them.

The Bond Market and

Treasury Yields

Key Point:

- Treasury and bond yields remain elevated as investors continued to consider the prospect of higher-for-longer interest rates.

During the second quarter both U.S. Treasury and bond yields remained elevated as investors assessed persistent inflation, resilient economic growth, and evolving expectations for Federal Reserve monetary policy. Throughout the quarter, the 10-year Treasury yield generally traded in the mid-4% range, while the 2-year Treasury yield remained above 4%, reflecting expectations that short-term interest rates would stay higher for longer. At the end of the second quarter, the 10-year Treasury yield closed at 4.44%, the 5-year Treasury at 4.19%, and the 30-year Treasury at 4.91%. (Source: U.S. Department of the Treasury Resource Center)

Bonds remain a core component of many well-balanced portfolios, and we will continue to monitor developments, Federal Reserve policy and Treasury markets as conditions evolve.

Oil

Key Points:

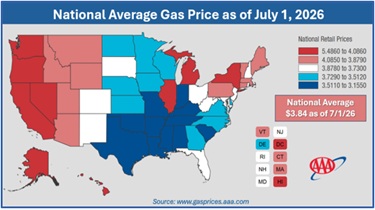

- National average gasoline prices increased nearly 32% in the second quarter of 2026.

- Easing geopolitical tensions late in the quarter contributed to a decline in crude oil and gasoline prices.

After averaging approximately $2.98 per gallon at the end of February, the national gasoline price average climbed to approximately $4.56 per gallon by mid-May. Higher crude oil prices, coupled with geopolitical tensions in the Middle East, contributed to the rise in fuel costs. (Source: gasprices.aaa.com)

As the quarter neared its end, oil prices dropped as geopolitical tensions eased. The global benchmark Brent crude fell below $73, after reaching April highs of over $125 per barrel. (Sources: cnn.com; bbc.com)

Investors’ Outlook

Key Points:

- We remain cautiously optimistic. While volatility is likely to remain, continued earnings growth, a resilient economy, and the possibility of a resolution in Iran, provide an encouraging backdrop for investors.

- Maintaining a long-term focus and avoiding short-term distractions has historically been an effective way to pursue financial goals.

As we enter the second half of 2026, the investment landscape remains, for the most part, positive, although investors should continue to expect periods of elevated volatility. The primary drivers of market performance are likely to still be; the direction of inflation, Federal Reserve policy, corporate earnings, geopolitical developments (particularly regarding the Strait of Hormuz), and confidence in advancements in technology and artificial intelligence.

Although volatility is expected, the combination of healthy corporate earnings and a resilient economy provides a supportive backdrop for investors as we move through the remainder of 2026. Most analysts are suggesting higher movements in equity markets for the remainder of 2026. Ed Yardeni, the highly respected President of market advisory firm Yardeni Research is forecasting a further 9% gain in the S&P 500. However, a handful of other analysts, including Tyler Richey, an analyst at Sevens Report Research, are predicting a decline in major indexes through the end of 2026. (Source: abcnews.com; 6/30/26)

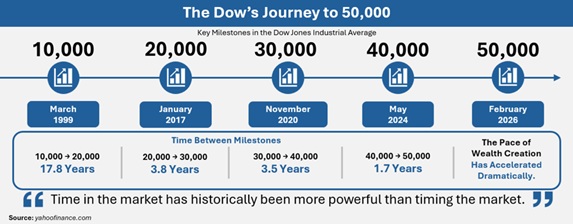

The pace of equity market growth has accelerated over the last decade and while we are not in the business of predicting the future, history has consistently demonstrated that maintaining a disciplined, diversified investment strategy remains one of the most effective ways to navigate uncertain markets. Rather than attempting to predict short-term movements or falling prey to the day-to-day noise from the media, investors are generally better served by remaining focused on their long-term financial objectives and allowing high-quality investments time to compound.

We will continue to closely monitor market developments and make thoughtful portfolio adjustments when appropriate, always with your long-term goals at the forefront of our investment decisions.

We believe an informed client is the best client and our team is here to help you with every step of your journey toward your financial goals. Please feel free to reach out to us with any questions or concerns you may have. We greatly value the trust and confidence you place in our firm and look forward to continuing to serve you.

Securities and advisory services offered through LPL Financial, a registered investment advisor. Member FINRA/SIPC

Note: The views stated in this letter are not necessarily the opinion of LPL Financial, and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. This information should be relied upon when coordinated with individual professional advice. This material contains forward-looking statements and projections. There are no guarantees that these results will be achieved. All indices referenced are unmanaged and cannot be invested in directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. There is an inverse relationship between interest rate movements and bond prices. note that individual situations can vary. This material contains forward-looking statements and projections. There are no guarantees that these results will be achieved. There is no guarantee that a diversified portfolio will enhance overall returns outperform a non-diversified portfolio. Diversification does not protect against market risk.

The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. The modern design of the S&P 500 stock index was first launched in 1957. Performance prior to 1957 incorporates the performance of the predecessor index, the S&P 90. Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stocks of companies maintained and reviewed by the editors of the Wall Street Journal. Past performance is no guarantee of future results. CDs are FDIC Insured and offer a fixed rate of return if held to maturity. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed.

Sources: Barron’s; apnews; statmuse.com; cnbc.com; gasprices.aaa.com; nytimes.com; cnn.com; bbc.com; investing.com; factset.com; yahoofinance.com; U.S. Department of Treasury. Contents provided by the Academy of Preferred Financial Advisors, 2026